The Economics of COSTCO - The Ultimate Subscription Business Disguised as a Retailer

- ohaiat

- May 3

- 5 min read

Executive Summary: The Membership Flywheel

Costco Wholesale ($COST) recently closed out an incredibly strong fiscal Q2 2026, delivering $68.24 billion in net merchandise sales (a 9.1% year-over-year increase). However, evaluating Costco on pure retail metrics completely misses the core economic engine of the company. Costco is not a traditional retailer; it is a subscription business that leverages immense scale to pass savings down to its members.

The real story of 2026 is the successful integration of their recent membership fee increase (raising Executive memberships to $130 and Gold Star to $65) alongside a massive acceleration in their digital transformation. With "digitally-enabled" sales surging 22.6% year-over-year in Q2, management is proving they can defend their physical moat while finally capturing the e-commerce growth that Wall Street has long demanded.

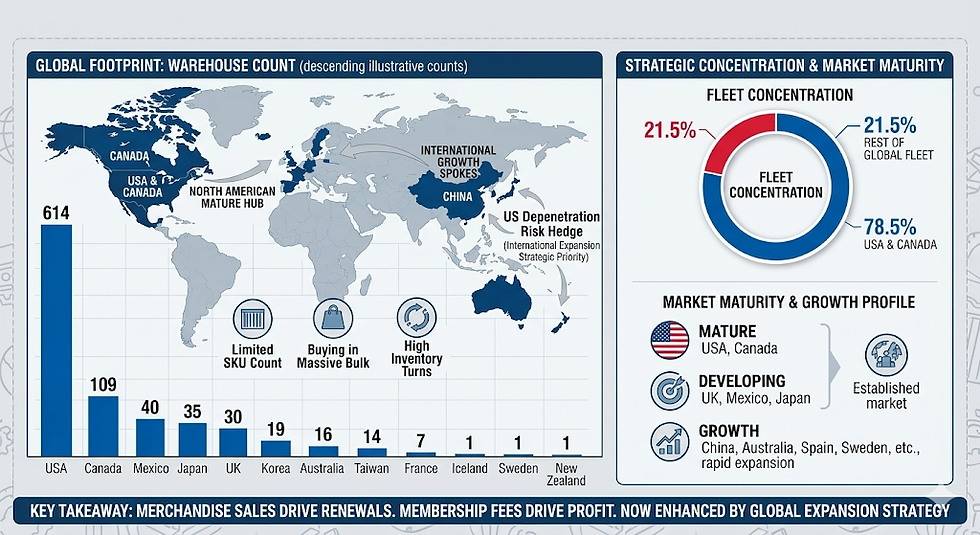

High-Level Background & Global Footprint

Operating 921 warehouses globally as of early 2026, Costco is one of the largest retailers in the world. Over 78% of its fleet is concentrated in the mature North American market (USA and Canada). The company operates on a beautifully simple premise: limit the number of SKUs (roughly 4,000 active items compared to a traditional supermarket's 30,000+), buy in massive bulk, and cap gross margins strictly around 14% to 15%.

Main Revenue Streams

To understand Costco’s financials, you must surgically separate the top line from the bottom line.

Merchandise Sales (The Volume Engine): This makes up roughly 98% of the company's total revenue. However, because Costco refuses to mark up products past a strict threshold, this division operates essentially as a break-even loss leader to drive renewals.

Membership Fees (The Profit Engine): This is the lifeblood of $COST. In Q2 2026 alone, membership fee income generated $1.36 billion (up 13.6% YoY). Because there is virtually no cost of goods sold associated with a membership fee, this high-margin recurring revenue accounts for the vast majority of the company’s operating income.

Analyzing the Business Model: The 1.8% Margin & Consumer Psychology

The Margin Reality: Q2 2026 vs. Q2 2025

To see the pricing discipline of Costco, we have to isolate the operating margin of the physical goods. In Q2 2026, Costco reported $2.60 billion in total operating income. If we subtract the $1.35 billion in pure-profit membership fees, we are left with a core merchandise operating profit of just $1.25 billion.

Dividing that by $68.24 billion in sales reveals a pure merchandise operating margin of exactly 1.83%. Looking back at Q2 2025, that exact same metric was 1.80%. This proves mathematically that even amidst supply chain fluctuations, management actively chooses not to pad their margins. They earn less than 2 cents of operating profit for every dollar of goods sold to ensure maximum value is passed to the consumer.

The Consumer ROI: Why Pay the Toll?

This incredibly low margin begs the ultimate behavioral economics question: Why do 82.1 million households pay a membership fee just to walk inside? Because the math dictates a guaranteed positive return on investment.

The Gold Star Breakeven ($65/year): Because Costco caps margins at ~14% (while traditional grocers run at 25%-30%), a consumer easily saves a conservative 10% on their bill. To break even on the $65 fee, a family only needs to spend $650 a year (about $54 a month). Most hit this on their second trip.

The Executive Breakeven ($130/year): Earning 2% cash-back, an Executive member breaks even at $3,250 a year. For a household buying weekly groceries and gas, the 2% reward check they receive at year-end routinely exceeds the $130 fee entirely, making the membership mathematically "free." Add in heavily subsidized gasoline (often 10-30 cents cheaper per gallon) and the trust placed in the Kirkland Signature label, and the consumer psychology shifts from paying a "toll" to unlocking an asset.

The International Moat: The "Glocalization" Strategy

As Costco rapidly expands its growth spokes into Asia and Europe, it is succeeding where rivals like Walmart have historically failed. Their secret weapon is "glocalization."

While the "bones" of the warehouse and major electronics brands remain identical worldwide, Costco aggressively localizes its food and grocery departments. Instead of forcing an American diet abroad, they integrate into the local culture.

In the UK, warehouses stock massive tubs of Marmite and Aberdeen Angus beef.

In Japan and Korea, the meat and seafood departments pivot to high-grade sushi platters and premium sliced beef tongue.

Even the legendary food court adapts—offering Poutine in Canada and Bulgogi bakes in Asia.

This local sourcing avoids the logistical nightmare of importing perishables and sheds the "arrogant American retailer" stigma, driving the high daily foot traffic necessary to secure international renewals.

Mapping the Business Risks

Despite its fortress-like balance sheet, the Costco flywheel is not invincible.

The Existential "Doom Loop": Costco’s superpower is its buying scale. If consumers ever decide the ROI is no longer positive and renewals drop, volume drops. Without volume, Costco loses the leverage to negotiate ruthless pricing with suppliers. Without those discounts, prices rise, destroying the value proposition and causing more members to leave. This is why maintaining a 92%+ renewal rate is an existential mandate.

Tariff & Geopolitical Exposure: With ongoing volatility in global trade policies, Costco faces immediate pressure on landed costs.

The Valuation Multiplier: Costco currently trades at a forward P/E ratio north of 50x. This is a software-like multiple for a company selling bulk groceries. The risk here is multiple compression; any slight miss on membership retention could trigger a severe market correction.

Competitor Landscape, SWOT Analysis & Conclusion

The Competitor Landscape

Sam’s Club (Walmart $WMT): The most direct competitor, often faster to adopt retail tech (scan-and-go), but lacking the premium demographic penetration of Costco.

Amazon ($AMZN): While Amazon Prime wins on convenience, Costco defends its moat with absolute unit pricing, high-ticket "treasure hunt" items, and bulk sizing.

SWOT Analysis

Strengths: Unrivaled pricing power; elite 92.8% U.S./Canada renewal rate; highly localized international merchandising.

Weaknesses: Razor-thin merchandise margins leave zero room for supply chain inefficiencies; priced for absolute perfection.

Opportunities: The 22.6% explosive growth in their digitally-enabled segment; rapid expansion in the Chinese and Australian markets.

Threats: Tariffs inflating merchandise costs; any macroeconomic shift that threatens the suburban household formation.

Final Conclusion: The Verdict on $COST

Wall Street consistently struggles to properly value Costco because it applies traditional retail frameworks to a business that operates completely differently. The company does not optimize for quarter-to-quarter gross margin expansion; it optimizes purely for member loyalty.

The seamless implementation of the 2026 fee hike proves that consumer demand for Costco's value proposition is highly inelastic. Furthermore, their mastery of international localization and their recent digital acceleration prove the business model scales globally and omni-channel. While the 50x P/E multiple is undeniably rich, $COST remains one of the most defensive, high-quality compounders in the market - a subscription powerhouse where the physical warehouses are simply the fulfillment centers for the membership fee.

Comments